Page 1 of 2

2 variables and 2 cointegrated eqns.

Posted: Fri Sep 09, 2011 6:31 pm

by dimitris

hi i am very new to e views and generally econemetrics and sorry for my silly questions. i have time series dara of inflation rate and unemployment. so there must be 0 or 1 cointegrated equations. my resutls on johansen coint. test on eviews are looking like that :

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None* 0.044691 25.9979 15.49471 0.0006

At most 1 * 0.039403 5.14570 3.841466 0.0233

Trace test indicates 2 cointegrating eqn(s) at the 0.05 level.

i know that it is possible to have 0 or 1 coint. equations and in that case i have 1 cointegrated equation. but why that is happening?it this wrong what is the excuse for this??is it linked whith the optimal lag length?

thnx in advance!!

Re: 2 variables and 2 cointegrated eqns.

Posted: Fri Sep 09, 2011 8:09 pm

by startz

hi i am very new to e views and generally econemetrics and sorry for my silly questions. i have time series dara of inflation rate and unemployment. so there must be 0 or 1 cointegrated equations.

Have you checked whether both series contain unit roots. A cointegration test doesn't make sense otherwise, and the standard US unemployment rate series is not integrated.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 4:57 am

by dimitris

both time series are integrated I(1) by ADF and PP .test. there are not stationary in their levels. it belgium harmonised unemployment,monthlydata. so now?? can u suggest me a good database with better data? i use oecd.

thnx in advance again

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 9:31 am

by startz

That's interesting. I wouldn't have expected unemployment to be I(1), so I've learned something.

Having said that, I think if you include a time trend in your ADF test you'll reject a unit root for unemployment.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 11:23 am

by dimitris

but my friend startz, i reject the unit root in the first differences.. that is the reason unemployment is I(1). right?? my problem is that i have 2 variables.. and eviews on johansen shows that i have 2cointegrated equation which is wrong bu the rule. because if u have 2 variables u should have maximum 1 cointegrated equation. (k-1) right??? correct me if i am wrong. because iam in start level on econometrics.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 11:57 am

by startz

If I'm following what you did, you haven't got it quite right. You want to test for a unit root in levels. This gets rejected for unemployment in Belgium if you include a time trend. The strong implication is that unemployment is I(0). (A test for unit root in first differences is a test of the null I(2) against the alternative I(1).)

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 1:13 pm

by dimitris

well. i have times series of belgium unemployment rate and inflattion rate as i said my friend.

the first step of cointegration is wheter each of these series are stationary or not! right??? ADF is applied to test stationarity for each of these series.

les take un=unemployment. if the value of the ADF statistic is less than the critical value at the conventional significance level then the series (un) is said to be stationary . If t UN is found to be non-stationary then it should be determined whether UN is stationary at first differences UN~ I (0) by repeating the

above procedure. If the first difference of the series is stationary than the series are integrated of order one , UN ~ I(1).If time series are I(1), than regressions is applied in their first difference. so by this i can procced to the johansen knowing that both series are I(1)/ right?? and the johansen test shows that i have 2 cointegrated equation which is wrong by the rule..

coorect me again if am wrong. and thku very much for the immediate responses!

Re: 2 variables and 2 cointegrated eqns.

Posted: Sat Sep 10, 2011 1:22 pm

by startz

well. i have times series of belgium unemployment rate and inflattion rate as i said my friend.

the first step of cointegration is wheter each of these series are stationary or not! right??? ADF is applied to test stationarity for each of these series.

les take un=unemployment. if the value of the ADF statistic is less than the critical value at the conventional significance level then the series (un) is said to be stationary .

The ADF has the null that there is a unit root. If the ADF statistic is low then you

don't reject the unit root. But myquick test (very quick test!) shows that the unit root is rejected.

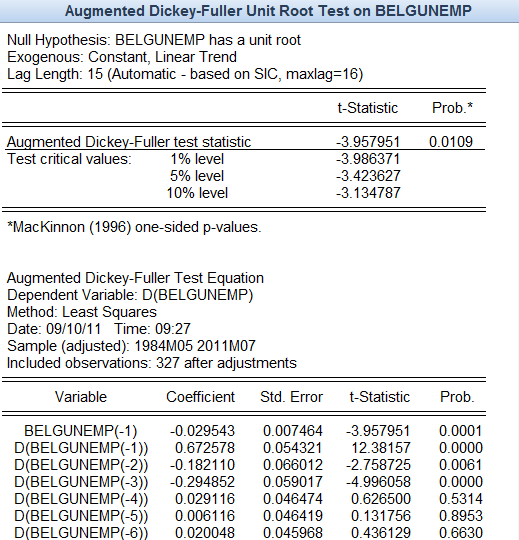

- Capture.PNG (39.56 KiB) Viewed 13711 times

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 5:31 am

by dimitris

well its ok for this but look at this. i have again unemplooyment and inflation rate by netherlands . so look

Null Hypothesis: INF has a unit root

Exogenous: Constant

Lag Length: 0 (Automatic based on SIC, MAXLAG=6)

t-Statistic Prob.*

Augmented Dickey-Fuller test -2.451766 0.1380

Test critica1% level -3.699871

5% level -2.976263

10% level -2.627420

*MacKinnon (1996) one-sided p-values.

Null Hypothesis: UN has a unit root

Exogenous: Constant

Lag Length: 3 (Automatic based on SIC, MAXLAG=6)

t-Statistic Prob.*

Augmented Dickey-Fuller test s -1.751735 0.3940

Test critica1% level -3.737853

5% level -2.991878

10% level -2.635542

Null Hypothesis: UN has a unit root

Exogenous: Constant, Linear Trend

Lag Length: 1 (Automatic based on SIC, MAXLAG=6)

t-Statistic Prob.*

Augmented Dickey-Fuller test -4.842860 0.0033

Test critical1% level -4.356068

5% level -3.595026

10% level -3.233456

so unemployment with constant only is not stationary. but with trend and constant is stationary in levels. inflation isnt stationary in levels. i check it with trend ,trend intercept.

so i have inflation which is stationary in first diffrences. and unemployment which is stationary with trend and intercept and not stationary only with trends.!! now how should i procceed to cointegration?? is it possible to procceed first of all? and somenhting else where did u get these series??

is there any good database to find unemployment and inflation stationary in fisrt diffreces to procced to cointegration and find one coint. equation???

thnx again!i hope that i dont tire u!i am gratefull to u bicause u helped me alot

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 7:45 am

by startz

I found the data series by following your suggestion! (Eurostat). I don't know whether you can find an I(1) unemployment series. There might be one, but it doesn't really make sense for unemployment to be I(1) as theory suggests that unemployment should gradually return to the natural rate.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 7:52 am

by dimitris

ok but if uemployment is I(0) how can i procced to cointegration ? i mean, what happens if unemployment is I(0) and inflation I(1?)??

also what happens if both of them are I(0)??

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 8:19 am

by startz

For two series to be cointegrated, they have to both be integrated of the same order. Otherwise the concept of cointegration doesn't apply.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 8:24 am

by dimitris

ok and if both series are I(0) can i proceed to johansen test? or not? if not what i have to do?

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 8:35 am

by startz

No. I(0) series cannot be cointegrated.

I'm not sure what you're trying to accomplish. If you could explain your objective, maybe someone here will have a suggestion as to another approach.

Re: 2 variables and 2 cointegrated eqns.

Posted: Sun Sep 11, 2011 12:02 pm

by dimitris

i want to do an emprirical investigation through causal analysis(granger) for the inflation and unemployment for a country ( not some specific country).

and the problem that i face problems is that i cant find countries whit inf and un stationary in first diffrences. more of them for example italy.etc, their inflation and unemployment are stationary in their levels. and i dont know what to do then. because i lack of knowledge in econmetrics!!