VAR exogenous variable shock

Posted: Tue Jul 12, 2022 9:23 am

by lotusfr

Hi there,

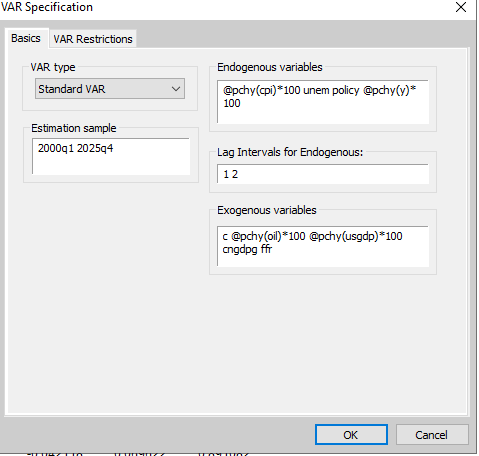

How to create IRF using exogenous variable shocks such as oil, USGDP and China GDP?

Thanks very much

Rong

- Capture.PNG (11.25 KiB) Viewed 7242 times

Re: VAR exogenous variable shock

Posted: Tue Jul 12, 2022 11:42 am

by random_user

It's possible to do this, but not easy. It can be done by imposing restrictions on the coefficients in the "VAR Restrictions" tab.

Essentially, you need to 1) add the exogenous variables as endogenous variables, and 2) make sure that, for the equation for the exogenous variable, all the lags on the coefficients of the lags of the other variables are forced to be equal to zero, and 3) make sure you either put the exogenous variables first (if you're using a Choleski identification) or impose a zero restriction of zero in the short-run impulse response matrix, such that the structural shocks over other variables don't affect your exogenous variable.

Re: VAR exogenous variable shock

Posted: Wed Jul 13, 2022 1:43 am

by lotusfr

It's possible to do this, but not easy. It can be done by imposing restrictions on the coefficients in the "VAR Restrictions" tab.

Essentially, you need to 1) add the exogenous variables as endogenous variables, and 2) make sure that, for the equation for the exogenous variable, all the lags on the coefficients of the lags of the other variables are forced to be equal to zero, and 3) make sure you either put the exogenous variables first (if you're using a Choleski identification) or impose a zero restriction of zero in the short-run impulse response matrix, such that the structural shocks over other variables don't affect your exogenous variable.

Hi thanks very much.

Could you please provide more details like a screenshot or how to do this using a program?

Re: VAR exogenous variable shock

Posted: Wed Jul 13, 2022 10:42 am

by EViews Matt

Hello,

Depending on what you're after, it may be easier to use a custom impulse vector that matches the effect of the exogenous variable. For example, the following code simulates a one unit shock to the exogenous variable z.

Code: Select all

wfcreate u 100

series x = nrnd

series y = rnd / 5 + .2

series z = rnd

var v.ls 1 2 x @pch(y) @ c z

matrix v_coefs = v.@coefmat

vector impulse = v_coefs.@row(6) ' This row holds the estimated coefficents on z.

v.impulse(imp=user, fname=impulse, se=none)