Page 1 of 1

DOLS - dynamic vs static forecasts

Posted: Wed Apr 06, 2016 10:47 pm

by maragloria

Hi there,

I'm running the following code to compare dynamic with static forecasts by running cointreg(dols):

Code: Select all

equation dols1_br.cointreg(method=dols, trend=const, lag=1, lead=1, cov=hac) reerln_br trdbal_br eff_totln_br @determ eff_rint_br

forecast reer_dyn

forecast(s) reer_lt

plot reerln_br reer_dyn reer_lt

dols1_br.resids(g)

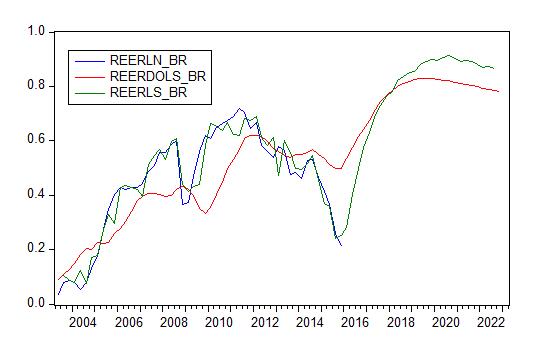

"forecast(s) reer_lt" is giving me the same values as "forecast reer_dyn" (see [img]

- graph1.jpg (21.57 KiB) Viewed 8611 times

[/img].

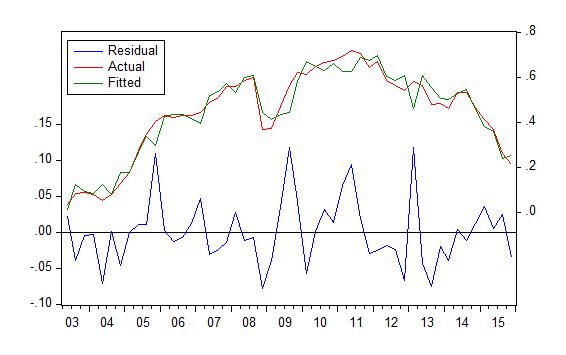

What I would like to get is the "fitted" in the graph below [img]

- graph2.jpg (27.67 KiB) Viewed 8611 times

[/img]. How can I get that?

Many thanks,

Mara

Re: DOLS - dynamic vs static forecasts

Posted: Thu Apr 07, 2016 3:15 am

by trubador

Use "fit" instead of forecast(s) to get static forecast. The latter is used in models containing ARMA terms and instructs EViews to ignore those terms and produce forecasts only for the structural part.

Re: DOLS - dynamic vs static forecasts

Posted: Thu Apr 07, 2016 6:32 am

by maragloria

Hello Trubador,

Thanks for your reply.

The problem is that "forecast reer_dyn" is not taking into account the dynamic term of the DOLS, as I thought it should. Is that so?

"forecast reer_dyn" and "fit reer_fit" gives the same forecasts.

See [img]

- graph3.jpg (21.93 KiB) Viewed 8595 times

[/img]

Warm regads,

Mara

Re: DOLS - dynamic vs static forecasts

Posted: Thu Apr 07, 2016 7:19 am

by trubador

That is because you are estimating a DOLS model, which produces forecasts only for the long term relationship that does not take into account the short term dynamics.

Re: DOLS - dynamic vs static forecasts

Posted: Thu Apr 07, 2016 7:32 am

by maragloria

I got the impression that the "fitted" in the graph with the residuals made using resids(g) do take into account the dynamic short-term term.

The "fitted" in graph 2 is quite different from the ones in graph 3 or graph 1.

Re: DOLS - dynamic vs static forecasts

Posted: Thu Apr 07, 2016 8:54 am

by maragloria

Indeed, I did an OLS regression specifying the dynamic term explicitly and its fitted value is quite similar to the one in the residuals graph of a DOLS regression.

See graph4 and graph 5 below.

[img]

- graph4.jpg (24.27 KiB) Viewed 8571 times

[/img]

[img]

- graph5.jpg (27.38 KiB) Viewed 8571 times

[/img]

My question is: is that a way for me to program a DOLS regression to get these fitted values (taking into account the dynamic term) given by the command resids(g)?

Many thanks,

Mara

Re: DOLS - dynamic vs static forecasts

Posted: Mon Apr 11, 2016 5:45 am

by trubador

I also cannot think of any other way to obtain dynamic forecasts other than explicitly specifying and estimating the model with OLS.