Page 1 of 1

Johansen Cointegration in Eviews

Posted: Sun Aug 16, 2009 4:21 pm

by Kalec

Hi

When I do the Johansen Cointegration test in Eviews, I see that the default setting was 1 to 4 lag interval.

Can anyone please tell me how to decide the number of lag interval to be used in EViews for this Johansen cointegration test?

Thanks and kind regards

Kalec

Re: Johansen Cointegration in Eviews

Posted: Mon Aug 17, 2009 2:58 am

by theologos

Hi,

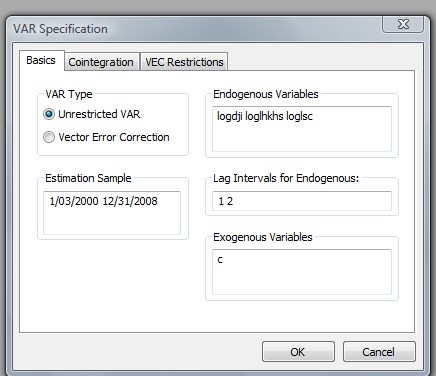

Initially run the VAR model of your interest without caring for the optimal lag structure. From the VAR window now select: view/ lag structure / Lag length criteria.

A new window appears where the Lag specification is desired. Specify the maximum lag length (depending on the frequency of your data) and press ok. After re-running the VAR model with the optimal lag length you may proceed to the Johansen cointegration approach.

Regards

Re: Johansen Cointegration in Eviews

Posted: Mon Aug 17, 2009 6:51 am

by Kalec

Thanks theologos

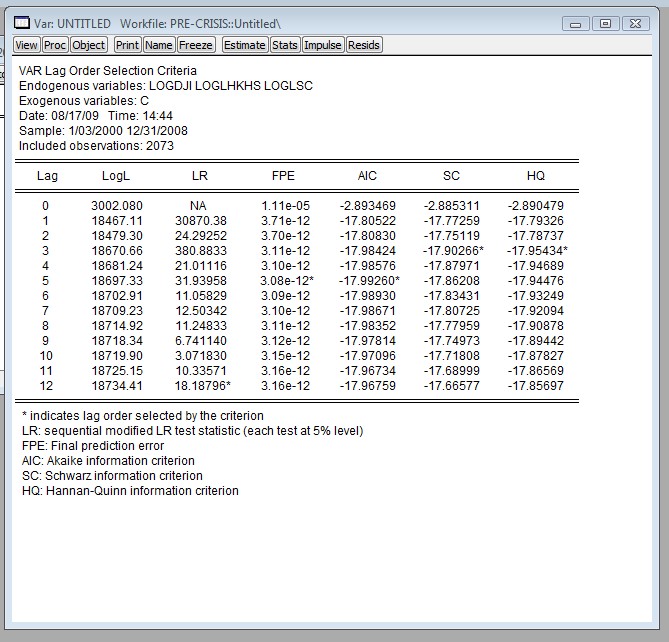

Below is the outcome from Eviews, and I noticed that the optimal lag length suggested by different criteria is different. I wonder which of the criteria should I rely more on? and how could I support myself relying on such criteria please?

- ScreenHunter_01 Aug. 17 14.44.jpg (30.54 KiB) Viewed 56037 times

- ScreenHunter_02 Aug. 17 14.45.jpg (113.31 KiB) Viewed 56030 times

Thanks

Kalec

Re: Johansen Cointegration in Eviews

Posted: Mon Aug 17, 2009 8:59 am

by theologos

Hi,

As you have realized there is no unique way to select the optimal lag length, therefore is quite easy to support your selection. Whenever multiple lag lengths appear two strategies can be followed:

1) Consider all the available criteria and let democracy to do the job

2) Choose one criterion (I usually choose the LR statistic)

Regards

Re: Johansen Cointegration in Eviews

Posted: Mon Aug 17, 2009 11:48 am

by Kalec

Thanks for your help theologos

Re: Johansen Cointegration in Eviews

Posted: Mon Jun 14, 2010 9:59 am

by cointthesis

I am also trying to determine the maximum lag length I should indicate for my lag length criteria test, and I was wondering if you could advise me.

I am examining daily (5 days a week) data from 2005-2010. What maximum lag length would be appropriate for such data, or how could I determine the most suitable maximum lag length?

Re: Johansen Cointegration in Eviews

Posted: Tue Dec 21, 2010 3:37 am

by wedira

Hi,

Initially run the VAR model of your interest without caring for the optimal lag structure. From the VAR window now select: view/ lag structure / Lag length criteria.

A new window appears where the Lag specification is desired. Specify the maximum lag length (depending on the frequency of your data) and press ok. After re-running the VAR model with the optimal lag length you may proceed to the Johansen cointegration approach.

Regards

Hi,

does it mean that I need to run VAR in levels, which aren't stationary (they are I(1)) and then:

1. I find the optimal lag length, then

2. I apply this lag lengt to Johansen cointegration test, then

3. I run VEC estimation with the number of lags and number of cointegrating vectors found in point 1. and 2.

Am I right?

Thanks in advance for your comments, regards

Re: Johansen Cointegration in Eviews

Posted: Fri Dec 24, 2010 11:56 am

by Arun.stat

Hi Wedira, you are done completely correct. As you said correctly to determine the optimal lag length, you need not make data stationary. This is because here you are not estimating the model coefficients. Non-stationarity matters in deriving the asymptotic properties (i.e. distribution, consistency etc.)of the estimators of coefficients, especially when underlying process is I(1)

HTH

Thanks,

Re: Johansen Cointegration in Eviews

Posted: Sun Mar 27, 2011 12:42 pm

by wedira

Thanks :)

how to?

Posted: Sun Apr 10, 2011 7:25 am

by dealsfe

how can i read Johansen cointegration test? i am a beginner. what should i read?

Re: Johansen Cointegration in Eviews

Posted: Fri Apr 15, 2011 10:36 am

by hgaronfolo

Hi,

I have used the method of I) estimating a VAR, II)View > lag structure > lag length criteria.

The lag selection indicates that I should use 8 lags. However, I am estimating my model on annual data, so 8 lags seems quite high, no?

The variables in my model are Market Capitalization and GNI.

Furthermore, if I increase the included lags in the lag selection to e.g. 12 lags, the lag selection will indicate that 12 lags is the best option. The optimal number of lags to include seems to go towards infinity, why is this? Can somebody explain this to me?

Thank you very much.

Re: Johansen Cointegration in Eviews

Posted: Tue Jun 11, 2013 3:36 am

by fboehlandt

Hello everyone,

I'm uncertain as to the validity of the approach suggested here. It is the purpose of a VEC to model the long-term cointegration relationship as well as susceptibility to short-term shocks at the same time. Thus, I'm not sure you can estimate the lag structure independent of the cointegration specification. You could calculate the IC for various lag lengths and deterministic trend assumptions and record the results in a matrix. However, I'm not sure if the IC are comparable. The only solution I have found to so far was to justify lag lengths on economic grounds. Someone mentioned the approach outlined in this thread is according to the EViews manual. Can anyone specify where? I was not able to find it. I would also appreciate any feedback on other solutions. Thanks

Johansen Cointegration in Eviews

Posted: Sat Sep 21, 2013 10:29 am

by Stephan122013

HI, I am running the Johansen cointegration tests on eviews. Can anybody show me the code to freeze the output table so I save some important elements in a matrix. I have 29 series for both items irq and srq.

I tried the following and it didn't work:

for !i=1 to 29

freeze(table) coint(a,4) irq_!i srq_!i

next

Thanks a lot!

Re: Johansen Cointegration in Eviews

Posted: Wed Jun 18, 2014 4:15 am

by vas001

Hi

I have uploaded a word file which may help you guys. Please let me know whether it helps you.

Vasanth Naik

Re: Johansen Cointegration in Eviews

Posted: Mon Jun 23, 2014 6:43 am

by wailycalcal

can anyone help me?

is there a long run relationship or not in time series data that i regress?(significant level=0.01)

one of independent variable is significant at 2nd difference while others are significant at 1st difference

should i use VECM, check the short run relationship using Granger causality test?