Page 1 of 1

URGENT ARDL interpretation Issue

Posted: Thu Jul 13, 2017 9:01 am

by Haim Rik

Hi Everybody,

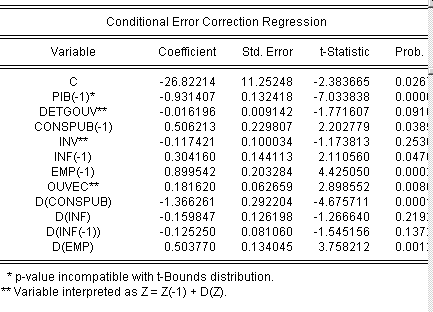

I'm performing an ARDL and I made "ARDL Long Run and Bound Test" with Eviews and juste after my "Conditional Error Correction Table", I got this message for some of my variables:

Variable interpreted as : Z = Z(-1) + D (Z)

So I'm not able to see the coefficient for example for Z(-1) to perform a Wald test for example and D(Z) to interpret for the short run the impact on my dependent variable.

How can I do to see these different coefficient ? Or How interpret ou understand that ? No effect on the short run?

Please I need an help

Aimeric

- Capture d’écran 2017-07-13 à 11.11.15.png (21.22 KiB) Viewed 22836 times

- Capture d’écran 2017-07-13 à 11.20.33.png (20.14 KiB) Viewed 22836 times

Re: URGENT ARDL interpretation Issue

Posted: Mon Jul 17, 2017 4:20 pm

by EViews Mirza

This just means that if your model has variables which are chosen to have zero lags, they have a special interpretation. In your particular case, for instance, the coefficient associated with INV** is -0.117421. The note basically says that:

-0.117421 INV** = -0.117421 INV(-1) -0.117421D(INV).

Accordingly, the coefficient estimate of INV(-1) is the same as that reported for INV**. I hope that clarifies the issue.

Re: URGENT ARDL interpretation Issue

Posted: Thu Aug 03, 2017 10:00 am

by NipNip

Does this mean that the coeficient of D(inv) is equal to zero?

-0.117421 INV** = -0.117421 INV(-1) + 0 D(INV).

Re: URGENT ARDL interpretation Issue

Posted: Thu Aug 03, 2017 10:23 am

by EViews Mirza

NipNip wrote:Does this mean that the coeficient of D(inv) is equal to zero?

-0.117421 INV** = -0.117421 INV(-1) + 0 D(INV).

No! It means the coefficient on D(INV) is the same as for INV(-1). In other words, -0.117421. I made that explicit in my previous post.

Re: URGENT ARDL interpretation Issue

Posted: Thu Aug 03, 2017 10:35 am

by NipNip

Thanks.

Re: URGENT ARDL interpretation Issue

Posted: Thu Aug 03, 2017 10:48 am

by NipNip

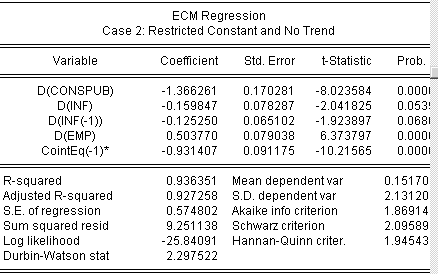

I've tried to do the ECM regression in excel, but I think I'm calculating the variable "CointEq" in a wrong way. I think I cannot follow what the equations say in ARDL chapter from Eviews user guide.

Please, can you guys help me with equation used to calculate "CointEq" variable?

I'm using Case 5: Unrestricted Constant and Unrestricted Trend.

Regards,

Joel

Re: URGENT ARDL interpretation Issue

Posted: Thu Sep 13, 2018 6:55 pm

by maymay

EViews Mirza wrote:This just means that if your model has variables which are chosen to have zero lags, they have a special interpretation. In your particular case, for instance, the coefficient associated with INV** is -0.117421. The note basically says that:

-0.117421 INV** = -0.117421 INV(-1) -0.117421D(INV).

Accordingly, the coefficient estimate of INV(-1) is the same as that reported for INV**. I hope that clarifies the issue.

in ecm regression, there is no estimation of D(inv). Does this means there's no short run impact for INV?

Re: URGENT ARDL interpretation Issue

Posted: Wed Sep 01, 2021 6:26 pm

by Hussen Alhwij

Thanks EViews Mirza for this explanation. It was very clear and useful. However, I would like to ask about conducting short run error correction based causality test. As the variables which selected to be zero lag will not appear in the short run model. In other words, how can we do wald test in this case.

Thank you very much