Thank you EViews Mirza, I have read these and they are very helpful.

The example I refer to can be found in this youtube example by Crunch Economics.

Many other authors on youtube follow the same method

https://www.youtube.com/watch?v=2F1OY_1X8A0.

In explaining it simply, I have added photors:

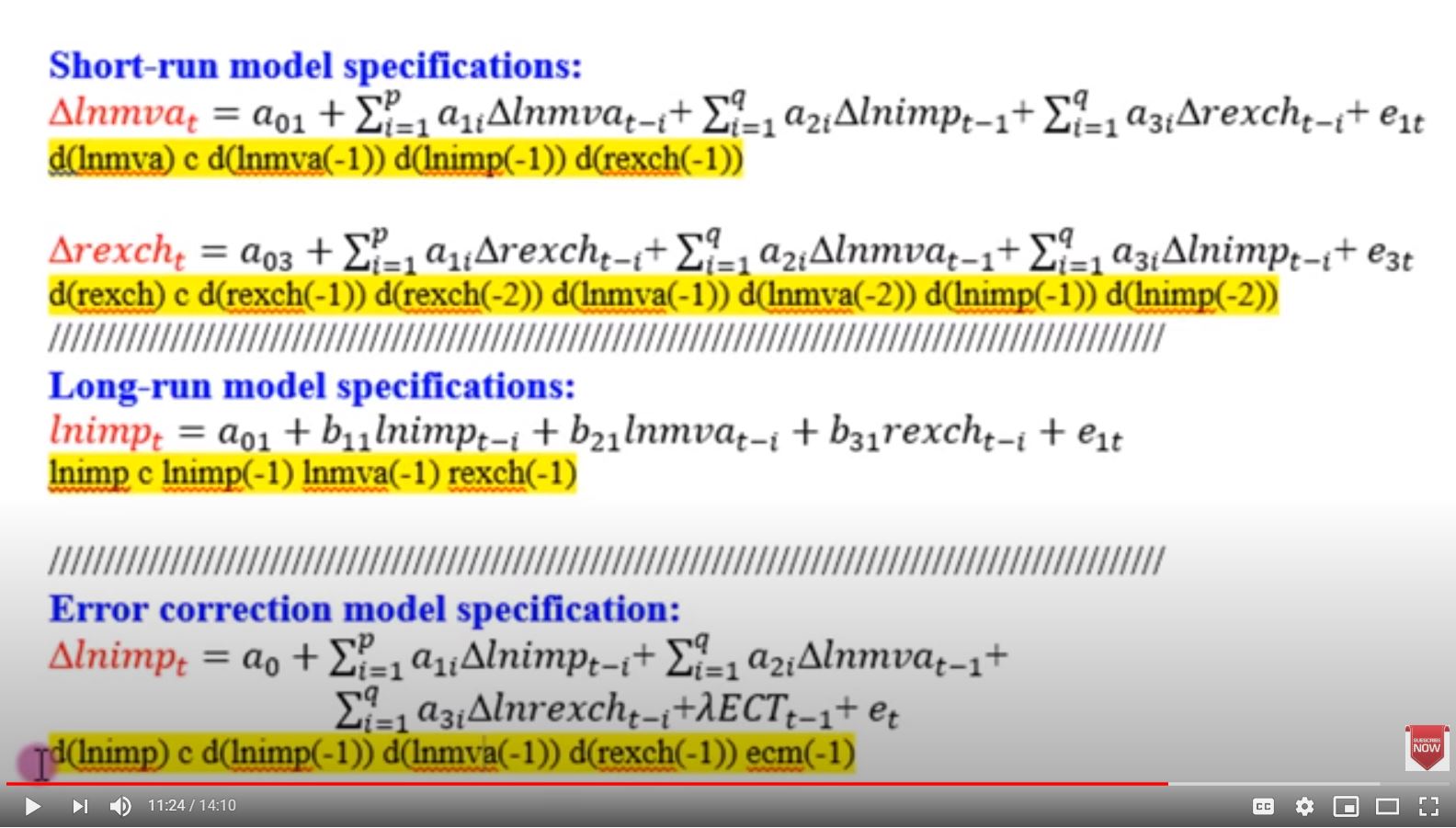

Photo 1: Shows the short-run and long-run model specifications used in the LS - Least Squares method.

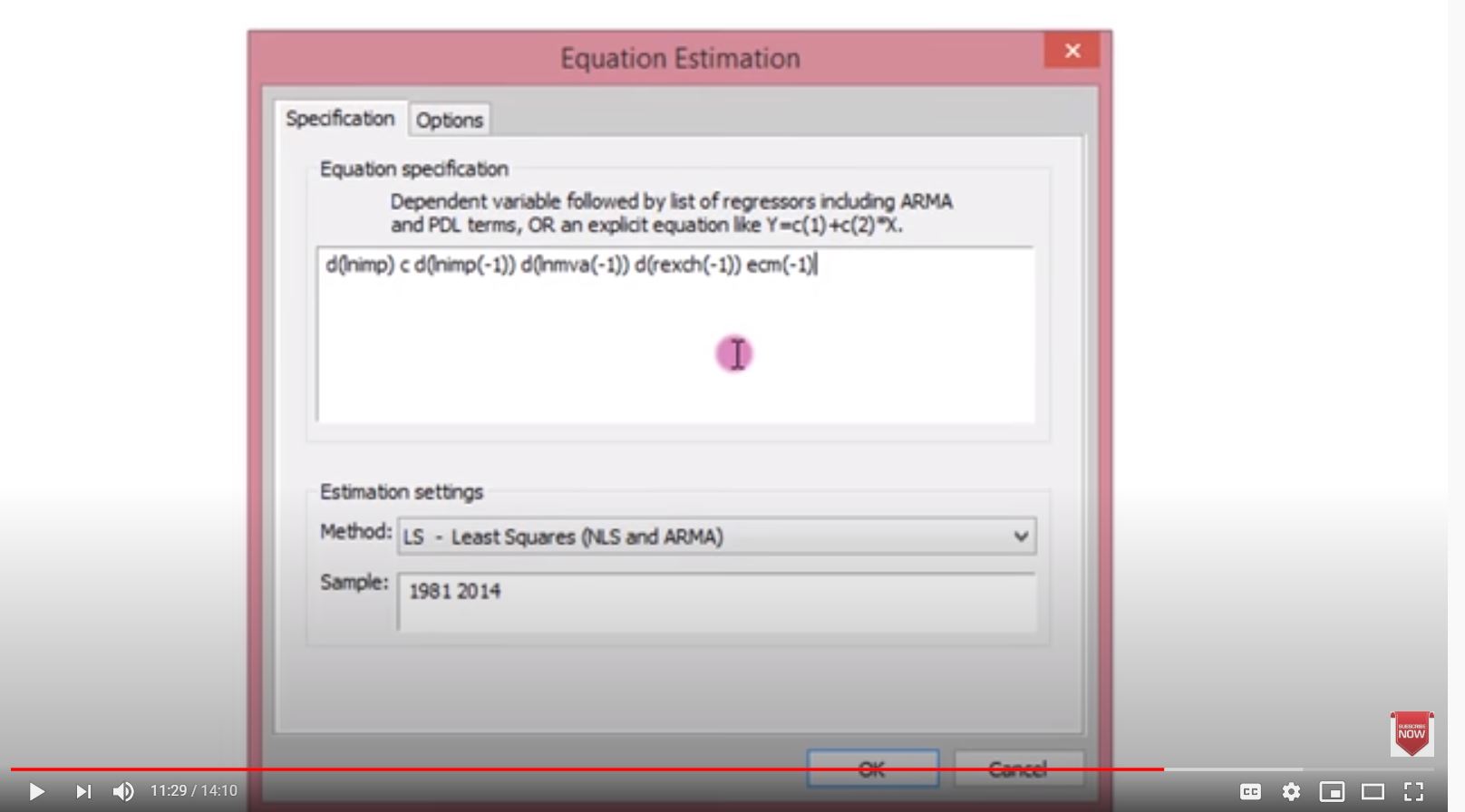

Photo 2: Using the long-run specification, you create the ECM series. Then you place in the LS equations (short run and long run) and run the model

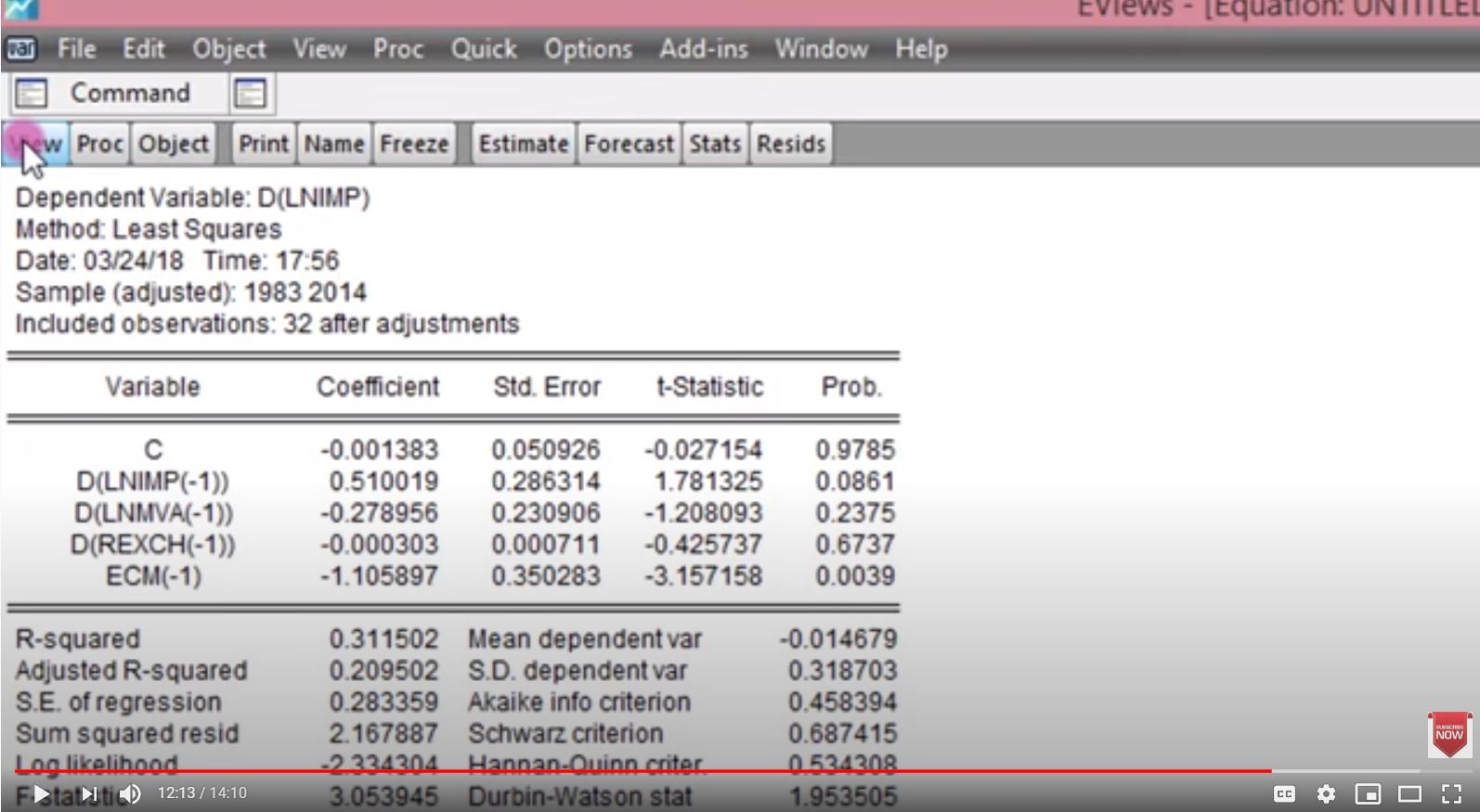

Photo 3: You run the short run and long run (EMC model) with the LS method. The ARDL-ECM model is then displayed

As you can see, this is a different method used.

Are you able to tell me why authors use this method?

My supervisor seems to think that the long-run model is not specified properly here.

If you did this method and compared it to the Eviews method (that we have spoken about), the long run model and ARDL contain different coefficients completely.

What are you thoughts?

- Photo 1.JPG (161.07 KiB) Viewed 18202 times

- photo 2.JPG (87 KiB) Viewed 18202 times

- photo 3.JPG (143.14 KiB) Viewed 18202 times