One of the most frequent questions we get regards the difference between AR(1) estimation and lagged endogenous variable estimation. Many people, it would seem, believe that the following two specifications should yield identical results (i.e. should give the same coefficient estimates for both the AR parameter and the constant):

Code: Select all

Y C AR(1)

Y C Y(-1)

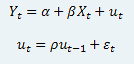

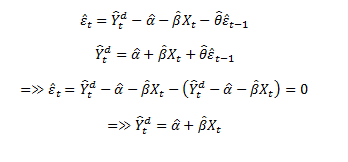

The confusion arises from the definition of an AR(1) Process. An AR(1) process is simply defined as Yt = c + rYt-1. Given this, is is easy to understand why people believe that estimation of Y with an AR(1) term is the same thing as estimation of Y on a lagged value of Y. However when you are estimating an AR equation, you are not saying that Y follows an AR process, rather you are saying that the error terms follow an AR process. This means that the specification is slightly different:

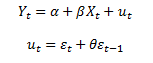

With some substitution you can re-arrange this specification to become:

or,

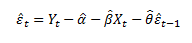

Clearly this is different from a regression of Yt on its lagged values:

since the coefficient on the constant is specified differently (although, obviously, you can go from one specification to the other with some simple algebra).

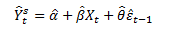

Note that the only difference between the two specifications is the coefficient on the constant. Everything else should remain the same.