Page 1 of 2

SVARpatterns

Posted: Fri Jan 31, 2014 2:03 am

by trubador

This thread is about

svarpatterns add-in for just-identified SVAR models.

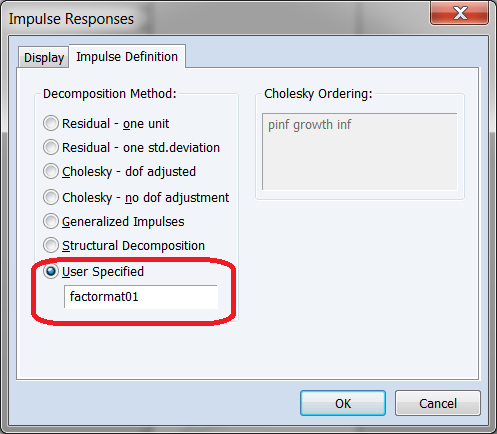

The add-in allows you to impose both short-run and long-run restrictions to obtain non-recursive orthogonalization of the error terms (as opposed to recursive Cholesky decomposition) for impulse response analysis that would make more sense from a macroeconomic/structural point of view. In order to use the add-in, you should first estimate a regular VAR model. After that, you can either supply the name of your model or the covariance matrix. The output will be a factor matrix, which

can further be used in generating impulse responses, but NOT in conducting variance decomposition (see the picture below). In short, this add-in aims to extend the current functionality of EViews' Structural VAR estimation toolbox.

- Use of factor matrix in impulse response

- Impulse_Response.png (29.04 KiB) Viewed 24474 times

Re: SVARpatterns

Posted: Sat Feb 01, 2014 3:48 pm

by terrya

Hi

Can this add-in be called inside a programme? I've searched the forum and googled in vain to find an answer to the more general question of whether add-ins can be called inside programmes rather like sub-routines.

Re: SVARpatterns

Posted: Sat Feb 01, 2014 4:01 pm

by EViews Gareth

Of course they can. Just use whatever command the add-in has assigned to it.

Re: SVARpatterns

Posted: Sat Feb 01, 2014 4:05 pm

by terrya

Thanks. I suppose I just missed this point somehow.

Re: SVARpatterns

Posted: Mon Feb 17, 2014 6:12 pm

by svar24

Does anyone know how to do variance decomposition after using SVARpatterns?

EViews only allow variance decomposition via Cholesky or structural decomposition (short OR long-run), but not when SVARpatterns is used.

Re: SVARpatterns

Posted: Sun Apr 27, 2014 9:02 am

by siarvey

How do i specify the long run and short run matices in the svarpatterns? e.g var1.svarpatterns(options).

Also, how do I do the impulse response functions after this?

Re: SVARpatterns

Posted: Sun Apr 27, 2014 2:39 pm

by siarvey

The options are clearly shown in the documentation. What is lacking now is how to do impulse response functions and variance decomposition after the svarpatterns. Any one has ideas?

Re: SVARpatterns

Posted: Sun Apr 27, 2014 2:44 pm

by EViews Gareth

You cannot.

variance decomposition in SVARpatterns

Posted: Wed Jan 14, 2015 9:08 pm

by ter_eviews

Hello

Is it possible to have the variance decomposition with the user specified factor matrix (the one obtained from LR and SR restrictions)??

Re: SVARpatterns

Posted: Sat Aug 15, 2015 2:31 pm

by Helia

Hello,

The SVAR add-in that help to estimate both short and long run restrictions, is it possible to have the variance decomposition?

And the output graphs, the dashed lines indicate a 95% confidence interval, or the one standard error bounds?

Re: SVARpatterns

Posted: Mon Nov 23, 2015 7:23 pm

by wilshire

Hi all,

When I use a matrix object (a variance-covariance matrix) to call the SVARpattersn addin, I got the following error message:

"Please supply the matrix for VAR coefficents."

Do you know how to fix it?

Thanks

Wilshire

Re: SVARpatterns

Posted: Tue Nov 24, 2015 2:11 am

by trubador

wilshire wrote:Hi all,When I use a matrix object (a variance-covariance matrix) to call the SVARpattersn addin, I got the following error message:"Please supply the matrix for VAR coefficents."Do you know how to fix it?ThanksWilshire

Please do not post the same question twice.

You need to explicitly provide the estimated VAR coefficients as a matrix as well.

Re: SVARpatterns

Posted: Tue Nov 24, 2015 6:25 am

by wilshire

Thanks Trubador.

I have another question: Almost every time when I run the addin, I got the error "Estimation not converge". But when I supplied a starting values matrix, I got another error which say "THETAVEC is not defined."

Can you please help?

Re: SVARpatterns

Posted: Tue Nov 24, 2015 2:36 pm

by trubador

Estimation from covariance matrix is a little bit complicated. I cannot locate the source of the problem without seeing the actual workfile. In the meantime, you can use the add-in through the VAR object, if possible.

Re: SVARpatterns

Posted: Wed Nov 25, 2015 6:45 am

by wilshire

Trubador,

Actually I used the VAR object to perform SVARPatterns. Please see attached the workfile. The VAR object is VAR_COMM, and pattern matrices are pattern_sr for short-run, and pattern_lr for long-run restriction. I have tried many ways to use the SVARPetterns but each time gives the error message "estimation not converges". I donot know why.

Wilshire