Page 7 of 11

Re: Fama-MacBeth regression

Posted: Tue Oct 21, 2014 10:40 am

by EViews Rebecca

Can you post the workfile you used?

Re: Fama-MacBeth regression

Posted: Tue Oct 21, 2014 10:30 pm

by fan

EViews Rebecca wrote:Can you post the workfile you used?

Thanks for the reply. This is my workfile. I am looking forward to hearing from you.

Re: Fama-MacBeth regression

Posted: Wed Oct 22, 2014 2:45 pm

by EViews Rebecca

Are you using "r*" to enter your portfolio returns in the add-in? In that case you will include the "resid" series, which you probably don't want to do. One solution is to rename the returns series to something that won't overlap with other series in your workfile.

Re: Fama-MacBeth regression

Posted: Wed Oct 22, 2014 8:33 pm

by fan

EViews Rebecca wrote:Are you using "r*" to enter your portfolio returns in the add-in? In that case you will include the "resid" series, which you probably don't want to do. One solution is to rename the returns series to something that won't overlap with other series in your workfile.

thanks for the reply.

Re: Fama-MacBeth regression

Posted: Tue Oct 28, 2014 1:15 pm

by fan

I am looking for help to implement following tests in the Fama-MacBeth regression. First, how can I include constant as a factor in the regression as many people do in their studies; second, how can I have the newey-west estimators from the time-series regressions and how can I test the joint significance of the loadings via SUR system; third, how can I have the t-statistics which are adjusted for errors-in-variables following Shanken (1992) and how can I have the adjusted R2 follows Jagannathan and Wang (1996) in the cross-sectional regressions. Thank you for your help

Re: Fama-MacBeth regression

Posted: Tue Oct 28, 2014 1:19 pm

by vickyzao

trubador wrote:First of all, make sure that you have EViews version 7.x or higher. Then, download the add-in and run the installation program (or simply unzip it). It will upload a documentation file into the related folder (C:\Users\...\Documents\EViews Addins\...), where you can find your answers.

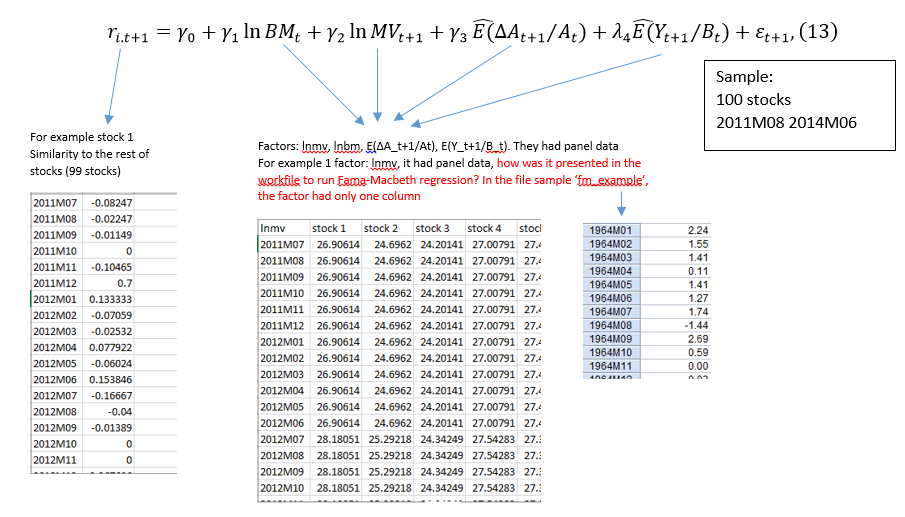

1 point that i could not understand in file "fm_example". For specific rmkt is a factor, it had value during the period, so these values corresponded with pr11 or pr12 ,..? What about for each portofilios/asset return. X is a factor, in general, X has panel data (for example 25 porfolios, 588 observations), how can it be showed in a sheet? . Could anyone help me how to present a factor in a workfile? Could you please tell me soon?

Thank you so much for your help.

Re: Fama-MacBeth regression

Posted: Tue Oct 28, 2014 2:23 pm

by EViews Rebecca

fan wrote:I am looking for help to implement following tests in the Fama-MacBeth regression. First, how can I include constant as a factor in the regression as many people do in their studies; second, how can I have the newey-west estimators from the time-series regressions and how can I test the joint significance of the loadings via SUR system; third, how can I have the t-statistics which are adjusted for errors-in-variables following Shanken (1992) and how can I have the adjusted R2 follows Jagannathan and Wang (1996) in the cross-sectional regressions. Thank you for your help

To answer your first question, look at equations 1 and 2 in the documentation. Your other questions are not covered by the add-in and you will need to do them yourself.

Re: Fama-MacBeth regression

Posted: Tue Oct 28, 2014 2:24 pm

by EViews Rebecca

vickyzao wrote:trubador wrote:First of all, make sure that you have EViews version 7.x or higher. Then, download the add-in and run the installation program (or simply unzip it). It will upload a documentation file into the related folder (C:\Users\...\Documents\EViews Addins\...), where you can find your answers.

1 point that i could not understand in file "fm_example". For specific rmkt is a factor, it had value during the period, so these values corresponded with pr11 or pr12 ,..? What about for each portofilios/asset return. X is a factor, in general, X has panel data (for example 25 porfolios, 588 observations), how can it be showed in a sheet? . Could anyone help me how to present a factor in a workfile? Could you please tell me soon?

Thank you so much for your help.

I don't understand what you're asking.

Re: Fama-MacBeth regression

Posted: Wed Oct 29, 2014 2:54 am

by vickyzao

I would talk my case in details. I had 100 asset returns (in 36 months), monthly returns were estimated a below picture

http://i1128.photobucket.com/albums/m486/vickyzao/myissue.pngTo use addin in Eviews, my workfile inclueded:

+ rm* (representative rm1, rm2,..., rm100: monthly returns of stock 1, 2, ...., 100) in 36 months

+ factors: lnBM, lnMV, E_A, E_Y, 4 variables

Hope this picture help you understand me

I am waitng for your reply

Thanks

Re: Fama-MacBeth regression

Posted: Wed Oct 29, 2014 1:17 pm

by EViews Rebecca

vickyzao wrote:I would talk my case in details. I had 100 asset returns (in 36 months), monthly returns were estimated a below picture

http://i1128.photobucket.com/albums/m486/vickyzao/myissue.pngTo use addin in Eviews, my workfile inclueded:

+ rm* (representative rm1, rm2,..., rm100: monthly returns of stock 1, 2, ...., 100) in 36 months

+ factors: lnBM, lnMV, E_A, E_Y, 4 variables

Hope this picture help you understand me

I am waitng for your reply

Thanks

The add-in does not handle factors that consist of multiple series.

Re: Fama-MacBeth regression

Posted: Thu Oct 30, 2014 11:55 am

by fan

Can anyone help me understand why I am getting this error message: "MATRIX-VECTOR INDEX IS OUT OF RANGE IN "VECTOR RETIC=@TRANSPOSE@ROWEXTRACT(RM,J))" ? Many Thanks

Re: Fama-MacBeth regression

Posted: Thu Oct 30, 2014 1:26 pm

by EViews Rebecca

Again, you need to post the workfile you're using.

Re: Fama-MacBeth regression

Posted: Wed Nov 05, 2014 2:51 pm

by fan

EViews Rebecca wrote:Again, you need to post the workfile you're using.

This is my work file. I am trying estimate returns on pm1 to pm10 and pr11 to pr55. I am not sure why I am getting the error message. Thank you

Re: Fama-MacBeth regression

Posted: Thu Nov 06, 2014 7:57 am

by EViews Rebecca

Works for me.

Re: Fama-MacBeth regression

Posted: Mon Nov 17, 2014 2:49 am

by ecofin

hi,

how can use GLS or GMM instead OLS in this add-in?

1-suppose that pr* and rmkt are autocorrelation i can modifie the code to add ar(1) in the end of equation, but the problem i lose one observation (nobs=587)

Code: Select all

equation {%subbetaeq}.ls {%subrets}(!i) c {%subfacs} ar(1)how can generate error equations (E(i)=c(i)*Ei(-1)) for each equations (pr11 c rmkt, pr12 c rmkt,...etc), and use the c(i) to transform the observation to make the first step of regression of Fama-Macbeth and show all equation in the spool objects resolt and importe the c(i) in the vector, and show the transformed series pr* and rmkt.

same problem with the second step if i add ar(1) in the end of equation i lose 1 observation (n=24)

Code: Select all

equation {%subcsavg}.ls avgrets c betag ar(1)2-how can make Fama-Macbeth with GMM?

{kind=link}