Kilian add-in

Posted: Tue May 28, 2019 3:21 pm

by dakila

This thread is about the

kilian add-in that that implements the Kilian bias-adjusted bootstrap for VAR impulse response.

Re: Kilian add-in

Posted: Thu Aug 08, 2019 3:44 am

by heer0

Hi guys,

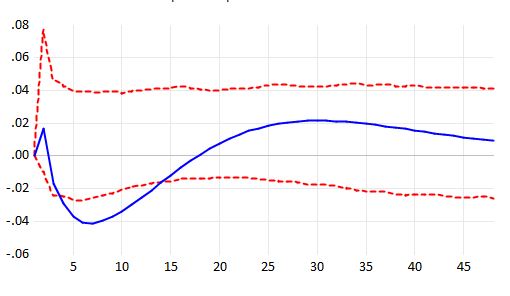

I have applied the Kilian add-in to a standard monetary VAR to retrieve impulse responses with bootstrapped confidence intervals. For a minority of impulse responses, the mean response exceeds the bootstrapped confidence intervals. To me, this does not make sense. For illustrative purposes, I will attach a picture of an impulse response to a monetary shock that exhibits said pattern.

I would be most grateful to you if you could provide me with possible explanations for this response behavior.

- IRF_Picture.JPG (25.34 KiB) Viewed 33296 times

Re: Kilian add-in

Posted: Tue Sep 10, 2019 12:39 am

by Wiz_Ven

Dear guys,

I have a problem with the Kilian add-in. I am running the code (the impulse variable is "dl_t_size") after a VAR estimation and it appears this error "Error 52 in encrypted program". My Eviews version is 11 updated to the last patch. Attached is the Eviews file. Thank you in advance.

Re: Kilian add-in

Posted: Wed Sep 11, 2019 12:04 am

by dakila

The bug is fixed. I hope the moderator will upload the add-in soon.

Re: Kilian add-in

Posted: Wed Sep 11, 2019 1:59 am

by EViews Gareth

Will be a week or so

Re: Kilian add-in

Posted: Sun Mar 01, 2020 2:58 am

by SilvioBerlusconi

Dear all,

thank you very much for providing this add-in. It is very useful.

I am wondering how can I obtain accumulated 'bands' when I use variables at the first-differences. The Kilian add-in (differently from the 'scale IRFs' add-in') cannot provided accumulated IRFs. I am wondering if it is sufficient to accumulate the bands provided by the Kilian add-in. are you going to implement this tool by allowing the add-in to accumulated directly IRFs and Bands?

Best,

S

Re: Kilian add-in

Posted: Sun Mar 01, 2020 6:09 pm

by dakila

I will try to include the option which provides the accumulative IRFs. Yes, you can do this manually after saving the IRFs or write code.

Re: Kilian add-in

Posted: Mon Mar 09, 2020 2:22 am

by SilvioBerlusconi

Thank you vary much for your help and effort.

I do not know neither the code for estimating the Kilian bootstrap in VAR models nor for estimating a 'scale factor for IRF'. The latter for instance is present in the Scale IRF add-in and not in the Kilian add-in.

Best,

S

Re: Kilian add-in

Posted: Sat Mar 27, 2021 5:29 am

by chris992

Hello Dakila,

I have recently downloaded the Kilian add-in and it works fine. The issue is that it only works on var objects. I am running a standard FAVAR monetary policy model following a Bank of England study (2015) code. At the last line, I end up with a matrix storing the impulse responses. I can see the graphs, but I cannot apply Kilian add-in to get bootstrapped standard errors. Is there any way we can modify the add-in or any code to obtain bootstrapped standard errors from matrices or vectors?

Thank you,

Chris

var favar.ls 1 2 pc1n pc2n pc3n pc4n pc5n pc6n pc7n pc8n pc9n pc10n CU_END_MONTH_OFFICIAL_BA

favar.impulse(12,g,matbys=irf) pc1n pc2n pc3n pc4n pc5n pc6n pc7n pc8n pc9n pc10n CU_END_MONTH_OFFICIAL_BA @ CU_END_MONTH_OFFICIAL_BA

matrix (158,11) weights 'creates matrix that will hold the proper weights

group pcn pc1n pc2n pc3n pc4n pc5n pc6n pc7n pc8n pc9n pc10n

matrix xx=@convert(pcn) 'new matrix containing the factors

scalar j

for j=1 to 105 'loop over the 105 slow-moving variables

'Left-hand side of the regression

matrix yy=@subextract(data,1,j,@rows(data),j) 'this sets up the j-th column of data for estimation

matrix btemp=@inverse(@transpose(xx)*xx)*(@transpose(xx)*yy)

weights (j,1)=btemp(1,1)

weights (j,2)=btemp(2,1)

weights (j,3)=btemp(3,1)

weights (j,4)=btemp(4,1)

weights (j,5)=btemp(5,1)

weights (j,6)=btemp(6,1)

weights (j,7)=btemp(7,1)

weights (j,8)=btemp(8,1)

weights (j,9)=btemp(9,1)

weights (j,10)=btemp(10,1) 'the previous linessave the weights

next

group pcn1 pc1n pc2n pc3n pc4n pc5n pc6n pc7n pc8n pc9n pc10n CU_END_MONTH_OFFICIAL_BA

matrix xx1=@convert(pcn1) 'matrix with factors and CU_END_MONTH_OFFICIAL_BA

for j=106 to 158 'loop over the 53 fast-moving variables

'Left-hand side of the regression

yy=@subextract(data,1,j,@rows(data),j) 'j-th column of data matrix

btemp=@inverse(@transpose(xx1)*xx1)*(@transpose(xx1)*yy)

weights (j,1)=btemp(1,1)

weights (j,2)=btemp(2,1)

weights (j,3)=btemp(3,1)

weights (j,4)=btemp(4,1)

weights (j,5)=btemp(5,1)

weights (j,6)=btemp(6,1)

weights (j,7)=btemp(7,1)

weights (j,8)=btemp(8,1)

weights (j,9)=btemp(9,1)

weights (j,10)=btemp(10,1)

weights (j,11)=btemp(11,1) 'note coefficients relating cu_int_rate and the data

next

'Impulse Responses

matrix irf1=@subextract (irf,1,111,12,121) 'irf of pc1n pc2n pc3n pc4n pc5n pc6n pc7n pc8n pc9n pc10n to CU_END_MONTH_OFFICIAL_BA shock

matrix irfmat=irf1*@transpose(weights)

P.S. I accidentally posted this to another thread Eqbootstrap (bootstrap standard errors). I am sorry about that!

Re: Kilian add-in

Posted: Fri Apr 02, 2021 2:56 am

by chris992

Hello,

On the same note, I have downloaded Eviews 12 and I was trying to run a VAR with user specified Decomposition method and apply Kilian's standard errors, but it says there is Internal error 500. I guess I can't apply both, is there a way to fix that or bypass that?

Thank you,

Chris