Page 1 of 1

Spectral Granger Causality Test*

Posted: Tue Jun 14, 2016 12:56 pm

by NicolasR

This add-in calculates a

Spectral Granger Causality Test based on Breitung and Candelon (2006), the test decompose the causality relations in the spectrum of frequencies which can be attributed to short run and long run causality relations. You can find the add-in help document and the example data attached.

Regards, Nicolas Ronderos Pulido

Re: Spectral Granger Causality Test*

Posted: Wed Jun 22, 2016 3:47 am

by trubador

I am not familiar with the methodology, but as I understand it does not have any problem with nonstationarity unlike its traditional time series counterpart. If I am not mistaken, this is one of the main advantages of working in the frequency domain. In any case, thanks for the effort and sharing.

Re: Spectral Granger Causality Test*

Posted: Thu Jun 23, 2016 3:18 pm

by NicolasR

Hi Trubador,

In the test you can apply the Toda and Yamamoto result. Nevertheless theoretically, to estimate a traditional spectrum conditions must be achived, some of them are related to a second order stationary process. By they way, great blog about your recent add-in, seems to be a better strategy to comunicate an add-in capabilities.

Best regards,

Re: Spectral Granger Causality Test*

Posted: Wed Aug 03, 2016 4:59 pm

by kAZbkh

thank you for this addin.

F- statistic didnt reported in results? only omega and P-values will be saved?

Re: Spectral Granger Causality Test*

Posted: Thu Aug 04, 2016 6:52 am

by NicolasR

Hi,

Yes, only the p-values and the frequencys are saved. For what do you need the statistical?

Regards,

Re: Spectral Granger Causality Test*

Posted: Tue Sep 13, 2016 7:07 pm

by cyp74

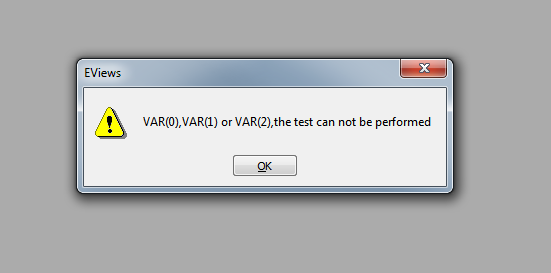

Thanks for the add-in. I occasionally get an error as attached. Any ideas why?

C.

- Capture.PNG (20.03 KiB) Viewed 50418 times

Re: Spectral Granger Causality Test*

Posted: Fri Sep 16, 2016 6:22 am

by NicolasR

Hi,

Because the test is based in two linear restrictions and you can not perfom a Wald (or an F) test if the number of restriccions in greater than the number of parameters, and since you are testing if the past of one variable (all its lags) at some frequency Granger-cause another variable 2>p where p is the lag order of the VAR(p). Suggestion: try with AIC criteria.

Best regards,

Re: Spectral Granger Causality Test*

Posted: Tue Nov 29, 2016 12:12 pm

by alphaomega

Hi,

I seem to be having a similar issue with the VAR Test error message. I'm not sure what I'm doing wrong since I'm just working with a very simple case between two data series, labeled series11 and series12 in the attached temp_data.WF1 file. Both series, as well as series21 and series22, are log differences of underlying data (and as log-differences are stationary). Any help/guidance would be greatly appreciated!

Thanks!

Re: Spectral Granger Causality Test*

Posted: Wed Nov 30, 2016 4:06 pm

by NicolasR

Hi,

You are not doing anything wrong, it is because what I mention in my previous post. You have two options, increase the maximum number lags or select the AIC criteria, in the case that any of this work ir means that a VAR(p) with p>2 it is not suggested to be fitted to the data and the test can not be performed.

Regards,

Re: Spectral Granger Causality Test*

Posted: Tue Dec 06, 2016 2:18 am

by jiangziyaok

i do not know what is meaning about the figure? how to test it whether pass the 5% significant test? i hope i can get help. thank you.

Re: Spectral Granger Causality Test*

Posted: Thu Dec 15, 2016 8:38 am

by NicolasR

If the p value of the test is under the significance level the hypothesis that a series X does not cause a series Y in the frequency wj is rejected. Also a graph with the label var1_var2 means that the variable var1 is the dependent and var2 the independent, therefore the hypothesis is that var2 does not cause var1 at frequency wj.

Regards,

Re: Spectral Granger Causality Test*

Posted: Thu Feb 09, 2017 7:33 pm

by alphaomega

Are you planning on adding the likelihood ratio (LR) statistic as an option for the lag selection criteria and/or the ability to manually set the lag length?

Thanks!

Re: Spectral Granger Causality Test*

Posted: Tue Feb 28, 2017 11:00 am

by NicolasR

The second suggestion would be more general for any lag desierd by the user, but the first will be easy to implement in the current version of the add-in. Thanks for the idea, I will see what I can do.

Regards,

Re: Spectral Granger Causality Test*

Posted: Wed Feb 24, 2021 2:02 am

by aawoad

Hello every one

Can I use this test for panel data?

Re: Spectral Granger Causality Test*

Posted: Wed Feb 24, 2021 8:40 am

by NicolasR

Hello,

In the orginal paper of Breitung and Candelon (2006), they develop the test in a time series context i.e. for VAR. I guess that it is not straigth forward to implement the test in a panel, maybe the add-in will run if you have panel data, but I would be very careful to interpret the results.

https://www.sciencedirect.com/science/a ... jp00wzyEfwRegards,