Hi guys! I'm a beginner student of econometrics and i need help. Once i have estimated a TGARCH(1,1), i have to answer the following question: " Insert in your best GARCH model the lagged daily range variable: is there any thing that changes? Is the sign of the daily range coefficient in line with your expectations? Please comment."

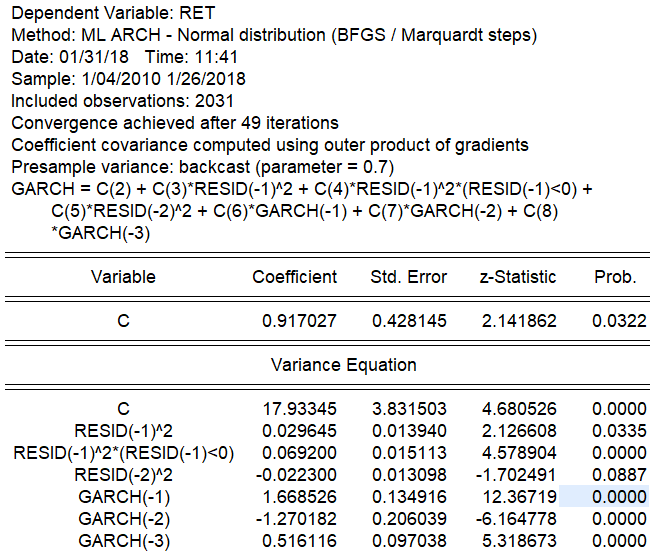

I produced i Eviews the following output:

- add lags.PNG (39.44 KiB) Viewed 1796 times

The thing i should comment is releted to the sign of the ARCH and the GARCH parts of the model. I notice that (for instance) GARCH(-1) is positive but GARCH(-2) is negative. Why?

Help me please

Thank you!